Non-Banking Financial Institutions (NBFIs) or NBFCs have become the backbone of the global lending ecosystem, particularly for underserved clients, including small entrepreneurs, salaried professionals, and rural borrowers. As the demand for NBFC loans grows, so does the need to modernize traditional, paper-heavy systems.

And there enter e‑Stamping and e‑Signing digital solutions that are transforming loan workflows into a faster, smarter, and far more customer-friendly process.

Do you know, resources claim, “In FY 2024-25, over 18 crore e‑stamp certificates were issued nationwide by SHCIL, evidencing broad uptake of digital stamp duty payment”

Don’t worry if you are still getting aware of these concepts! In this blog, we’ll explore why digitizing, stamping, and signing are critical, how they deliver value, and what steps NBFIs can take to embrace change without overwhelming themselves. Let’s delve into the concept!

The Obstacles in Traditional Loan Processes

Imagine this: A borrower, excited to fulfill a lifelong dream, seeks NBFC loan services. They visit an office, wait in line, fill forms manually, buy physical stamp paper, sign documents in person, and then wait days for verification. Doesn’t every step only depict the delays or errors, whether it’s a missing signature, an illegible stamp, or courier delays? For the borrower, it feels tedious, and for the NBFIs, it’s costly and prone to risk.

- Lending is no longer reliant solely on manual stamping and signature collection, as they have always clashed with customers’ expectations.

- Today’s modern customer wants everything quicker, smarter, and more flexible so that they can use it anytime on their phone.

- Along with this, even the regulators rightly demand strict audit trails, consent briefs, and compliance records.

This shows the high time to outgrow the conventional lending patterns and instill digital lending setups for NBFIs.

What are e-Stamping and e-Signing?

Before we explore how e-stamping and e-signing work in the NBFC loan process, let’s understand these tools:

- e‑Stamping

A government-authorized method for paying stamp duty online. Once paid, a unique e-stamp certificate is generated instantly, complete with an encrypted QR code and reference number.

- e‑Signing

A secure digital signature process that authenticates documents online. Consider it as a digital version of “wet ink,” but faster, safer, and auditable.

Together, they eliminate the need for physical paperwork, branch visits, a courier, or buying stamp sheets. Everything happens instantly, across devices, preserving legality and clarity. This helps both NBFCs and customers with an efficient lending process, building credibility, and quick fund access.

Why Is It Important to Integrate e-Stamping & e-Signing Into the NBFI Loan Process?

But as we learn about these impactful tools in the digital lending industry, what makes it important for NBFCs/NBFIs to integrate them into their NBFC loan management system? Let’s discuss:

1. Speed & Efficiency

In the fast-paced world, time for people is one of their biggest assets! With e‑Stamping, stamp duty is paid and acknowledged in seconds. e‑Signing is equally smooth; you send the document, the customer signs via OTP or identity proof authentication, and it’s done.

Compare that with traditional processes:

| Traditional Method | Time Taken | Risk Points |

| Buying stamp paper | Hours / Days | Wrong value, stock shortage, counter error |

| Cottage signature loops | Days / Weeks | Courier delays, document loss, illegible stamping |

| Manual audits | Weeks | Audit escape, missing pages, paper tampering |

By contrast, digital stamping and signing bring down the timeframes from days to minutes, while removing five or more clashing points such as lengthy forms, poor onboarding experience, complicated verification proves, and more in the process.

2. Security, Traceability & Compliance

Stamp duty is a legally essential part of the digital lending process. But paper-based stamping is vulnerable to fraud, mistakes, and forgery. On the other hand, e‑Stamping is issued by authorized providers and logged in encrypted registries. The resulting documents carry unique IDs that can be verified instantly online.

Similarly, e‑Signing creates an audit trail, timestamp, signer identity, and signature metadata that are embedded in the document. No complication, missing signatures, or compliance gaps.

However, let’s learn about the primary concern, that how it simplifies the NBFI loan process!

How e-Stamping & e-Signing Empower the NBFC Loan Process

In the lending industry, especially within NBFCs and NBFIs, even small operational hurdles can turn into major customer dissatisfaction or regulatory risk. This is why embracing e‑Stamping and e‑Signing doesn’t just make processes faster but also fundamentally improves how an NBFI functions across all critical dimensions. Let’s break this down into three core benefit areas and understand why they matter.

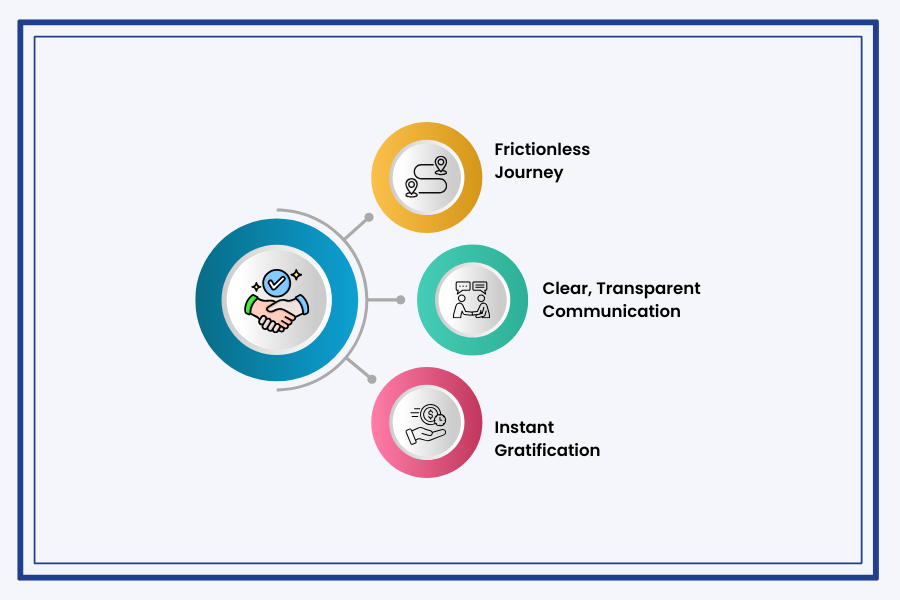

1. Borrower Experience: Faster, Simpler, and Trustworthy

The biggest win is how borrowers feel about the lending process. In today’s digital-first world, customer expectations are shaped by instant food delivery, 24/7 e-commerce access, and seamless app-based services. Traditional NBFI processes, with paperwork, multiple visits, and physical signatures, simply don’t align with this pace and modern expectations. Hence, here’s how digital stamping and signing are transforming this experience:

- Frictionless Journey: From application to agreement signing, borrowers complete the entire process on their phone or laptop. It requires no physical meetings or waiting for couriered papers. Everything happens at their convenience, flexibly.

- Clear, Transparent Communication: Each document signed comes with audit stamps, a secure QR-coded e‑Stamp, and a digital trail. Borrowers know exactly what they’re signing, when, and why. This works as an essential trust-building factor for NBFIs.

- Instant Gratification: No more “Your loan is in process.” With stamping and signing done instantly, loan disbursal happens faster, facilitating borrowers and enhancing your brand’s reputation.

Borrowers today not only value the faster, smarter, yet reliable services, in fact they also share them with their knowns. Word-of-mouth plays a huge role in NBFC growth, and streamlined digital processes create those exceptional experiences that customers love to share.

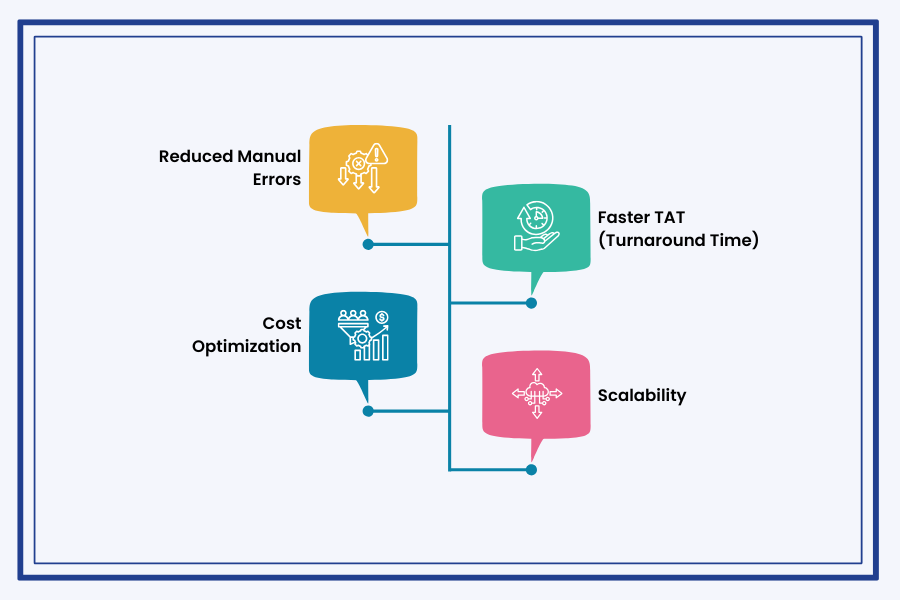

2. Operational Gains: Scalable, Error-Free, and Cost-Efficient

NBFC operations are traditionally resource-intensive. Managing stamp paper inventory, coordinating physical signature collection, and handling document storage all cost time, money, and human effort. However, they are also severely prone to high errors and compliance risks, auditing, and customer trust. Digitizing this workflow offers substantial gains, such as:

- Reduced Manual Errors: Digital stamping ensures exact denomination and correct authoritative command, while e‑Signing platforms ensure no missing or mismatched signatures. It results in significantly reduced processing errors and contract rejections.

- Faster TAT (Turnaround Time): A contract that would’ve taken 3-5 business days to get signed and stamped now closes in 30 minutes or less. This dramatically increases the number of loans an NBFI can process per day, without increasing team size.

- Cost Optimization: No paper, no courier costs, no physical storage or retrieval issues. Digitization slashes document-handling costs and improves process rate, unlocking growth without added expenses.

- Scalability: As your NBFI grows, manual processes can’t keep up with the modern requirements. Digital systems scale with ease and allow you to handle 10x the volume with minimal additional operational load.

Eventually, you’re not just saving resources but also reconfiguring your operations to be future-ready, flexible, smarter, and ready to scale.

3. Risk & Compliance Control

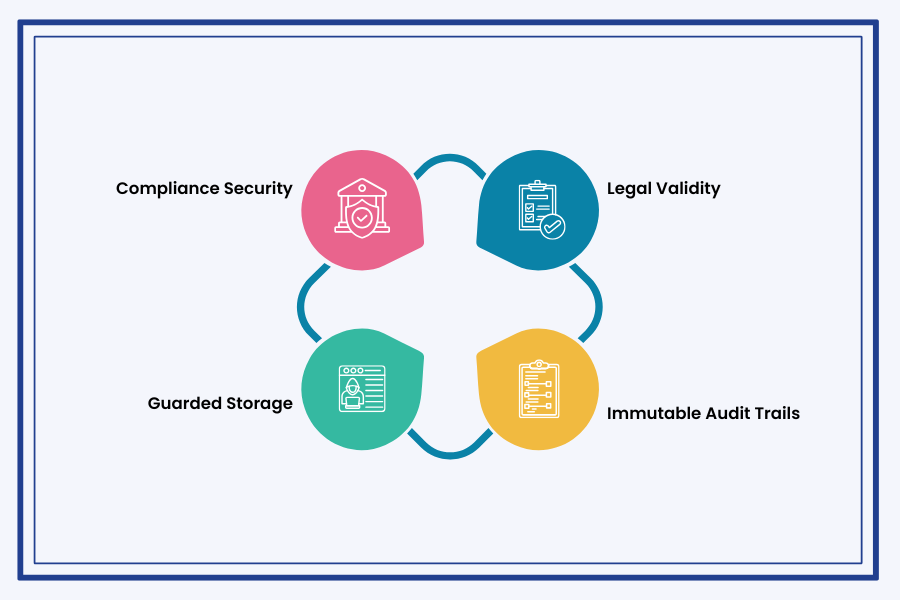

In financial services, even a small compliance miss can foster massive challenges. Regulators expect NBFCs to demonstrate clear documentation, verified borrower consent, and legal validity at every step. Traditional, paper-based systems often make this hard to enforce consistently. One missing page or an unsigned clause can cost you money, reputation, and your customer’s trust. Here’s where digital stamping helps NBFIs by:

- Legal Validity: Both e‑Stamping and e‑Signing are legally recognized under the Indian Stamp Act and the Information Technology Act. Nations like the US (under the ESIGN Act) and the EU (through eIDAS regulations) legally recognize electronic signatures, ensuring they hold the same enforceability as handwritten ones, if audit trails, consent, and data integrity are maintained. That means the contracts you generate carry the same legal significance as traditionally signed and stamped papers, only with added security and traceability.

- Immutable Audit Trails: Every action is recorded, including when the document was signed, where, on which device, and by whom. This level of detail is crucial for internal audits, customer dispute resolution, and regulatory inspection.

- Guarded Storage: Digital documents, once stamped and signed, are stored on encrypted servers with restricted access and backup redundancy. No risk of paper damage, misplacement, or manual misfiling.

- Compliance Security: When your NBFC handles hundreds or thousands of contracts daily, standardization is what works incredibly well. Digital processes enforce uniformity, ensuring every document is formatted, stamped, and signed exactly to policy.

Final Words

E-Stamping and e‑Signing are not just regular tech innovations, but also the foundation of modern, customer-centric NBFC lending. They allow NBFCs to offer an immaculate lending experience to customers. On one hand, borrowers get speed, convenience, and clarity; on the other hand, NBFIs get compliance, cost-saving, and brand trust.

In fact, by integrating this robust foundation with AI in financial services, NBFCs can potentially shift from analog paper processes to a dynamic, intelligent credit machine. A system with smarter underwriting, frictionless execution, and adaptable scalability.

For any NBFI aiming for ensured future growth, having e-stamping & e-signing in their NBFC loan management software is mandatory. And if you’re ready to integrate this NBFC business loan setup into your lending structures, all you need is a reliable partner like Lendmantra. Our experts help you with e-stamping, e-signing, and other NBFC loan services and solutions that can help your business foster scalability, acquire market space, and customer trust. To know more about how we can be your efficient partner, connect with our experts now!

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

Are e-stamped and e-signed documents legally valid in India?

Yes, e-stamped and e-signed documents are legally valid in India.

e‑Stamping is authorized by the Indian Stamp Act and facilitated through platforms like SHCIL. e‑Signing is governed by the Information Technology Act, 2000, and is accepted by courts, regulators (including RBI), and government bodies as equivalent to physical signatures.

What are the key benefits of implementing digital stamping and signing for NBFCs?

- Faster loan disbursals with reduced turnaround times

- Cost savings on paper, courier, and manual operations

- Higher compliance with audit-ready, tamper-proof documents

- Improved borrower experience through 100% remote, mobile-first processes

- Scalability, allowing NBFCs to process high volumes with fewer resources

How secure is the process of e-stamping and e-signing for financial transactions?

Both e‑Stamping and e‑Signing use industry-grade encryption and secure authentication methods (like Aadhaar OTP, digital signature certificates). Every document carries a unique ID, timestamp, and audit trail, ensuring integrity, non-repudiation, and traceability. These systems are designed to meet banking-level security standards.

Which government-approved platforms support e‑Stamping in India?

The Stock Holding Corporation of India Limited (SHCIL) is the central agency authorized by the Government of India to implement e‑Stamping in multiple states. States also designate state-specific authorized collectors (ACs) and vendor-integrated platforms via SHCIL APIs for NBFCs and fintechs to integrate e‑Stamping directly into their systems.