India’s lending ecosystem has changed dramatically over the last few years. What once involved lengthy paperwork, multiple branch visits, and slow approvals has now become a seamless digital experience powered by technology. From instant approvals to paperless onboarding, digital lending platforms are transforming how borrowers access credit.

For non-banking financial companies (NBFCs), this shift has opened exciting opportunities. With advanced digital lending solutions, lenders can now serve customers faster, reach underserved markets, and improve operational efficiency. The growing use of AI in financial services has made this transformation even more powerful, enabling smarter risk analysis and faster decision-making.

But rapid innovation comes with an important question: can NBFCs remain compliant while scaling digitally?

As regulations continue to evolve under the guidance of the Reserve Bank of India, staying regulatory-ready is no longer optional. Compliance is now a critical part of sustainable growth in digital lending.

This blog explains the key compliance requirements and how NBFCs can stay regulatory-ready in India’s evolving digital lending landscape.

- The Rise Of Digital Lending In India

- Why Compliance Has Become A Top Priority?

- Who Must Comply With Digital Lending Regulations?

- Key Compliance Areas NBFCs Must Focus On

- The Biggest Compliance Challenges For NBFCs

- How Technology Can Strengthen Compliance?

- Best Practices For Staying Regulatory-Ready

- Final Thoughts

- Frequently Asked Questions

The Rise Of Digital Lending In India

India has emerged as one of the fastest-growing digital credit markets globally. Increased smartphone penetration, improved internet access, and digital payment adoption have made borrowing more accessible than ever before.

Today’s borrowers expect convenience. They want quick approvals, transparent processes, and flexible repayment options. Traditional lending models often struggle to meet these expectations, which is why NBFCs are increasingly adopting modern digital lending solutions.

Technology has changed the lending journey in several ways:

- Instant customer onboarding

- Automated eligibility checks

- Faster credit assessments

- Digital documentation

- Real-time loan tracking

The use of NBFC loan software has allowed lenders to streamline internal operations while improving customer experience.

At the center of this transformation is AI in lending, which enables institutions to process large volumes of data and make informed credit decisions within minutes.

Why Compliance Has Become A Top Priority?

As digital lending expands, so do regulatory expectations. Regulators are focused on ensuring that borrowers are protected from hidden charges, unfair recovery practices, data misuse, and a lack of transparency. The digital nature of modern lending introduces risks related to cybersecurity, privacy, and third-party integrations.

For NBFCs, compliance is about much more than following rules. It directly impacts:

- Customer Trust

Borrowers are more likely to engage with lenders who offer clear terms, transparent pricing, and secure digital experiences. - Business Reputation

Non-compliance can damage market credibility and affect long-term customer relationships. - Operational Stability

Regulatory breaches may lead to penalties, audits, restrictions, or operational disruptions.

As digital lending platforms become more competitive, compliance is increasingly becoming a differentiator.

Who Must Comply With Digital Lending Regulations?

Digital lending regulations apply to a wide range of entities involved in the lending ecosystem. These include:

- NBFCs offering loans through digital lending platforms

- Banks partnering with fintech companies

- Fintech firms acting as Lending Service Providers (LSPs)

- Digital lending apps (DLAs) facilitate credit services

Whenever a lending product is offered through an app or online platform, these financial entities must comply with RBI digital lending guidelines. This includes ensuring proper data usage, customer protection, and transparency in loan terms.

For NBFCs that rely heavily on loan origination system technology and automated underwriting tools, compliance must be built directly into the platform architecture.

Key Compliance Areas NBFCs Must Focus On

To stay regulatory-ready, NBFCs need to pay close attention to several critical compliance areas.

1. Transparent Loan Disclosures

Borrowers must receive complete and accurate information before accepting a loan.

This includes:

- Interest rates

- Processing fees

- Penalty charges

- Repayment schedules

- Total borrowing cost

A strong loan origination system helps automate these disclosures, ensuring consistency and reducing manual errors.

When customers understand exactly what they are agreeing to, disputes become less likely.

2. Data Privacy and Consent

Modern lending relies heavily on customer data.

From income verification to transaction history, digital lenders process large amounts of sensitive information. Regulations increasingly require lenders to collect only necessary data and obtain clear borrower consent.

Using a secure loan management system infrastructure helps NBFCs:

- Track customer consent

- Store data securely

- Monitor access controls

- Maintain audit trails

As AI in financial services grows, responsible data governance becomes even more important.

3. Fair Recovery Practices

Digital convenience should never come at the cost of ethical recovery processes.

NBFCs must ensure recovery methods remain professional, transparent, and compliant with evolving standards.

Automated reminders and borrower communication systems within digital lending solutions can improve collections while maintaining professionalism.

4. Direct Fund Disbursal

Regulatory frameworks increasingly emphasize direct fund transfers between lender and borrower accounts.

This improves accountability and reduces misuse of intermediary structures.

A well-integrated loan management system ensures these processes are monitored and documented efficiently.

The Biggest Compliance Challenges For NBFCs

While the path to compliance is clear in principle, execution can be difficult.

Many NBFCs face operational and technological hurdles that make compliance management complex.

- Frequent Regulatory Updates

Financial regulations evolve quickly. What worked last year may require adjustments today. Keeping up with policy changes can be resource-intensive, especially for smaller lenders.

This is where adaptable NBFC loan software becomes valuable. Systems that allow quick policy updates help institutions stay aligned without major disruptions.

- Legacy Systems

Many NBFCs still rely on outdated infrastructure. Manual workflows, disconnected tools, and limited automation make compliance monitoring difficult.

Without a modern loan origination system, even basic compliance tasks can become slow and error-prone.

- Third-Party Dependencies

Many digital lenders partner with fintech service providers for onboarding, analytics, collections, and payment processing.

While these partnerships accelerate innovation, they also introduce compliance risks.

NBFCs remain accountable for ensuring that all partners follow regulatory standards.

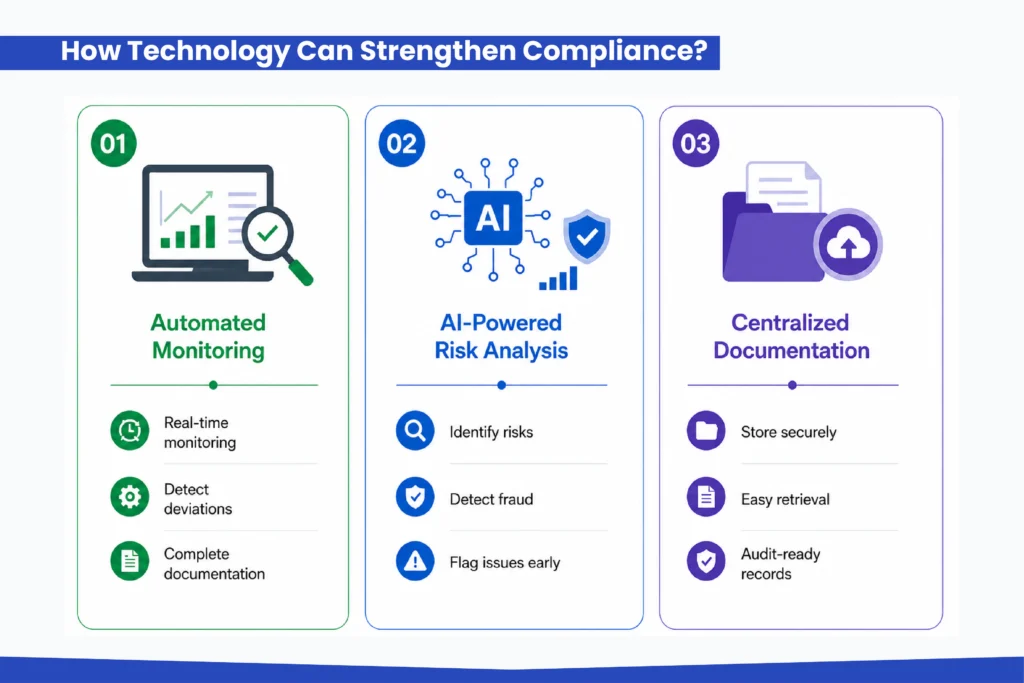

How Technology Can Strengthen Compliance?

The good news is that technology itself can solve many compliance challenges.

The same digital transformation driving growth can also create stronger governance.

1. Automated Monitoring

Modern loan management system platforms can monitor lending workflows in real time.

This allows lenders to detect:

- Missing disclosures

- Process deviations

- Unauthorized access

- Incomplete documentation

Automation reduces human error and improves consistency.

2. AI-Powered Risk Analysis

The role of AI in lending goes far beyond credit scoring.

AI can help identify unusual borrower behavior, detect fraud patterns, and flag compliance risks before they escalate.

This makes AI in financial services an important tool for proactive compliance management. When implemented responsibly, AI improves both efficiency and regulatory control.

2. Centralized Documentation

Regulatory audits often require detailed documentation.

A digital-first system ensures that every transaction, approval, consent form, and communication is stored in one accessible environment.

This is where advanced digital lending solutions create real value. With centralized records, NBFCs can respond quickly to audits and inspections.

Best Practices For Staying Regulatory-Ready

Compliance should never be treated as a last-minute checklist.

The most successful NBFCs build compliance into their operational foundation.

- Build a Compliance-First Culture

Every department should understand the importance of regulatory adherence. From customer service to technology teams, compliance must be a shared responsibility.

- Invest in Modern Infrastructure

A scalable loan origination system and efficient loan management system create the backbone for compliance. Technology investments reduce risk while improving speed and accuracy.

- Conduct Regular Audits

Internal audits help identify gaps before regulators do. Routine assessments ensure systems remain aligned with current standards.

- Train Teams Continuously

Regulations evolve, and teams must evolve with them. Regular training helps employees stay informed about new requirements and best practices.

Final Thoughts

Digital lending has created enormous opportunities for NBFCs to expand reach, improve efficiency, and serve customers better. But growth without compliance is risky.

To stay regulatory-ready, NBFCs need the right combination of technology, governance, and adaptability. Investing in advanced loan origination system tools, scalable loan management system platforms, and responsible AI in lending capabilities can help lenders meet both customer expectations and regulatory standards.

In today’s fast-moving financial landscape, compliance is no longer just about avoiding penalties. It is about building trust, ensuring sustainability, and creating a stronger future for digital finance.

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

What Is The Role Of Loan Service Providers (LSPs) In Digital Lending Compliance?

The LSPs act as an intermediary to manage the process of onboarding, KYC, and servicing. The NBFCs are still accountable for compliance, which includes monitoring LSPs' compliance with regulations, data protection, and transparency.

How Do Audit Trails And Reporting Systems Help NBFCs Remain Regulatory-Ready?

An audit trail records all transactions and decisions made in the system. It ensures transparency. Reporting systems assist in the preparation of compliance reports, audits, and error reduction. It helps NBFCs respond quickly to regulatory checks and requirements.

What Practices Should NBFCs Follow To Build A Digital Lending Ecosystem?

NBFCs can implement AI-based secure digital lending platforms, automation of compliance, data secrecy, standardization, monitoring of partners, and transparency to create a scalable platform.