The lending industry has always been built on conversations. A borrower walks into a branch, explains a need, negotiates terms, and seeks reassurance before signing. For decades, that human exchange shaped trust. Since AI bots came, the channel has changed, but the principle has not.

Today, the most effective lenders understand that borrower engagement is no longer defined by branch visits or even call centers. It is shaped by conversational AI, intelligent, responsive systems that speak, listen, guide, and resolve in real time across apps, websites, WhatsApp, and voice interfaces.

From application to repayment, AI in lending is redefining how borrowers experience financial services. The result: faster decisions, fewer drop-offs, better repayment behavior, and stronger lifetime value.

Let’s examine how this transformation is unfolding in 2026 in this blog post.

- What Do Digital Borrowers Expect from Lenders?

- How Conversational AI Transforms the Loan Lifecycle

- How Does Multilingual Conversational AI Improve Financial Inclusion?

- Simplifying Compliance and Documentation with AI Assistance

- How Conversational AI Drives Growth and Intelligence?

- Conversational AI in Lending: The Road Ahead

- Final Words

- Frequently Asked Questions

What Do Digital Borrowers Expect from Lenders?

Modern borrowers do not “apply” for loans. They compare, simulate, check eligibility, calculate EMIs, and expect near-instant decisions.

In mature digital lending platforms, borrowers expect:

- Instant eligibility checks

- Transparent documentation guidance

- Real-time status tracking

- Flexible repayment conversations

- 24/7 access without waiting on human agents

Traditional scripts and static FAQs cannot meet this demand. This is where conversational AI solutions become critical.

Unlike rule-based chatbots of the past, 2026 systems interpret intent, respond contextually, and integrate directly with backend systems such as loan originating software and loan management software for nbfc institutions.

The difference is profound: instead of navigating menus, borrowers have a conversation.

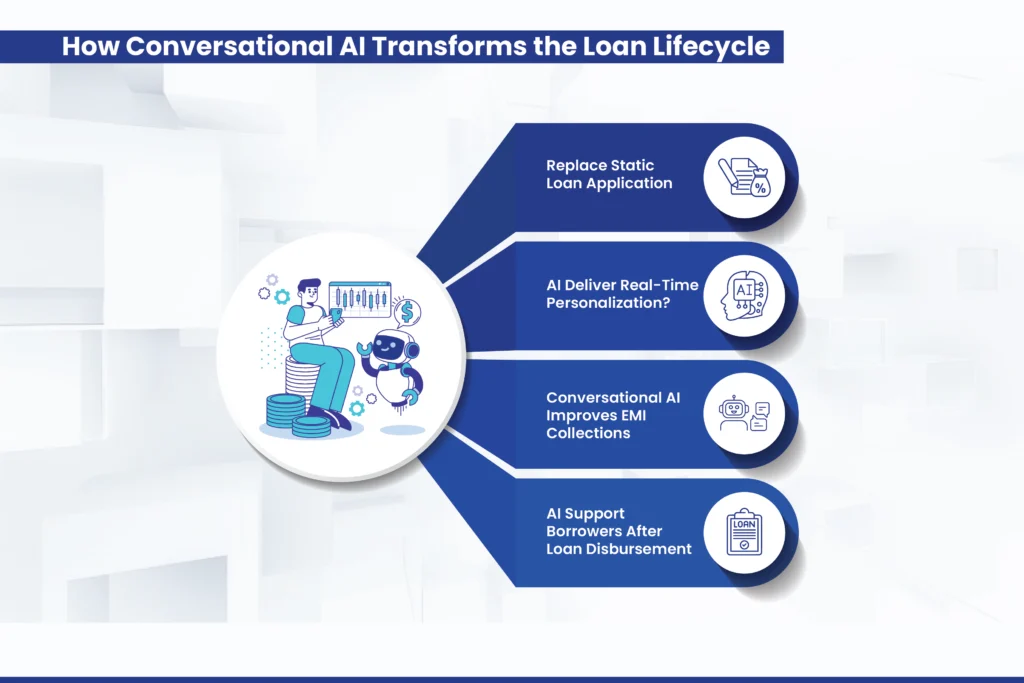

How Conversational AI Transforms the Loan Lifecycle

1. Replace Static Loan Application

In earlier digital lending solutions, borrowers were asked to go through long forms. Any confusion often led to abandonment. In 2026, the application process feels like a guided dialogue. For example: The borrower asks, “Can I get a ₹5 lakh business loan?”

- The system checks eligibility instantly.

- It asks for missing data conversationally.

- It explains interest structures clearly.

- It adapts questions based on responses.

This integration between conversational AI and loan originating software reduces friction at every step of the application and other lending processes.

2. AI Deliver Real-Time Personalization?

Personalization used to mean adding a borrower’s name in an SMS. In 2026, personalization is predictive and contextual. With AI in lending, systems analyze repayment history, credit behavior, transaction patterns, and interaction history. Through conversational AI solutions, borrowers receive:

- Tailored loan top-up suggestions

- Context-based EMI reminders

- Personalized restructuring options

- Intelligent cross-sell prompts

For NBFCs using advanced loan management software, this integration ensures the system “remembers” each borrower’s journey. When a borrower asks, “Can I reduce my EMI this month?”, the system calculates eligibility in real time using connected NBFI loan management software and offers structured options. The experience feels human because it is context-aware.

3. Conversational AI Improves EMI Collections

Instead of repetitive calls, borrowers receive empathetic nudges through chat or voice. The system:

- Detects early signs of stress

- Offers payment rescheduling

- Explains penalties clearly

- Automates settlement conversations

Integrated with loan management software for NBFC, these systems ensure compliance while maintaining dignity. The use of AI in lending for predictive delinquency analysis also enables proactive communication. Borrowers are contacted before they miss a payment rather than being connected after a missed EMI. This subtle shift enhances engagement and improves portfolio performance simultaneously.

4. AI Support Borrowers After Loan Disbursement

Borrower engagement does not end at disbursement. In fact, retention begins there. Modern digital lending solutions use conversational AI to maintain ongoing dialogue:

- EMI reminders with dynamic repayment links

- Balance summaries on request

- Instant foreclosure calculations

- Top-up eligibility checks

Through integration with NBFI loan management software, borrowers receive real-time answers without waiting for customer support. This constant accessibility builds trust. Trust builds loyalty. Loyalty drives repeat borrowing.

How Does Multilingual Conversational AI Improve Financial Inclusion?

One of the most powerful contributions of conversational AI solutions in 2026 is linguistic accessibility.

India’s lending ecosystem spans diverse geographies. Traditional digital lending solutions struggled with regional language support. Now, advanced digital lending platforms deploy voice-enabled conversational AI in multiple Indian languages.

Borrowers can:

- Ask questions in Hindi, Tamil, Marathi, or Bengali

- Upload documents guided by voice instructions

- Clarify repayment queries without confusion

This integration with loan originating software ensures that inclusion is not symbolic; it is operational.

Financial literacy improves when systems communicate in the borrower’s language. Engagement increases because understanding increases.

Simplifying Compliance and Documentation with AI Assistance

Compliance complexity remains a major bottleneck in lending. Missing documents, incorrect uploads, and unclear KYC instructions delay approvals. In 2026, AI in lending eliminates this friction through guided document assistance.

Integrated with digital lending platforms, conversational AI solutions:

- Validate uploaded documents instantly

- Flag missing data clearly

- Explain regulatory requirements in simple language

- Reduce back-and-forth communication

When connected to loan management software for NBFC, document verification becomes part of a seamless workflow. This way, borrowers are not overwhelmed; they are guided.

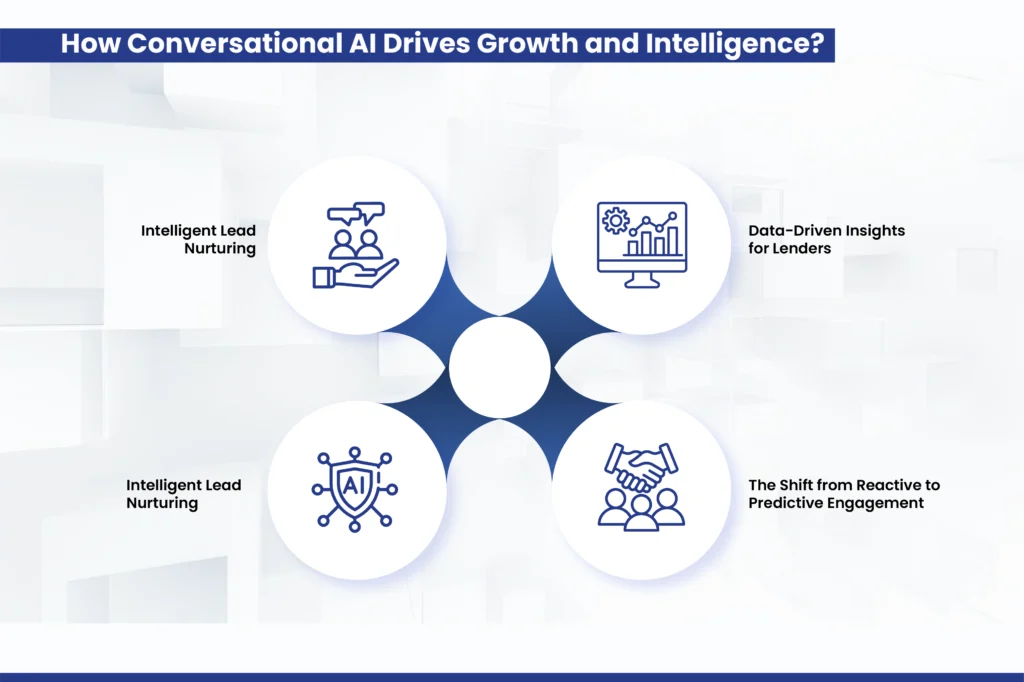

How Conversational AI Drives Growth and Intelligence?

1. Intelligent Lead Nurturing

Borrower engagement begins before application. On websites and mobile apps, conversational AI acts as an intelligent financial advisor. It evaluates user behavior and provides contextual nudges such as:

- “You may qualify for a lower interest rate.”

- “Based on your profile, documentation required is minimal.”

- “Pre-approved offers available, would you like to check?”

By connecting to backend loan-origination software, these systems generate real-time eligibility insights. For non-banking financial institutions, deploying NBFI loan management software means higher-quality leads entering the funnel. Instead of cold inquiries, lenders receive informed, engaged prospects.

2. Data-Driven Insights for Lenders

While borrower engagement improves on the front end, the backend benefits equally. With AI in lending, every borrower interaction becomes structured data. Lenders gain insights into:

- Common application drop-off points

- Frequently asked compliance questions

- Payment deferral trends

- Customer satisfaction patterns

Connected to a dynamic loan management software for NBFIs (non-banking financial institutions), these insights drive product refinement. In 2026, competitive advantage lies not just in capital deployment but in engagement intelligence

3. The Shift from Reactive to Predictive Engagement

Earlier systems responded to borrower queries. Today’s conversational AI solutions anticipate them. For example:

- A borrower nearing credit utilization limits receives pre-approved upgrade suggestions.

- A customer showing irregular repayment behavior receives structured guidance before delinquency.

- Seasonal cash-flow borrowers receive timely top-up offers.

Through deep integration with digital lending platforms and NBFI loan management software, predictive engagement becomes automated and scalable.

4. Security, Privacy, and Ethical AI

As AI in lending grows, so does regulatory scrutiny. In 2026, compliance is built into the architecture of conversational AI systems. Modern digital lending solutions incorporate:

- End-to-end encryption

- Consent-based data access

- Transparent decision explanations

- Bias monitoring frameworks

This ensures that automation enhances fairness rather than undermines it. When deployed responsibly alongside robust loan originating software, conversational AI solutions improve both efficiency and accountability.

Conversational AI in Lending: The Road Ahead

The evolution of AI in lending is far from what it is expected to be in the future. Voice biometrics, sentiment analysis, hyper-personalized underwriting, and adaptive repayment models are rapidly maturing.

However, one principle remains constant: lending is built on trust. Technology cannot replace that trust, but it can strengthen it.

When conversational AI solutions are deeply integrated with loan originating software, digital lending solutions, and NBFI loan management software, the borrower experience becomes frictionless, transparent, and responsive.

The institutions that master this integration will define the next phase of financial growth.

Final Words

As borrower expectations rise, lenders require more than standalone tools. Sustainable engagement now depends on integrated ecosystems that combine conversational intelligence with operational depth.

When conversational AI is seamlessly connected with loan origination systems, loan management software, and digital lending platforms, engagement becomes structured, proactive, and measurable. Borrowers experience clarity and responsiveness, while lenders gain visibility, control, and predictive insight.

For NBFCs and banks, the opportunity lies not just in automation, but in intelligent orchestration — where every borrower interaction is connected to backend decision-making and portfolio strategy.

The institutions that successfully align engagement technology with core lending infrastructure will be better positioned to improve portfolio performance, enhance borrower trust, and scale responsibly in an increasingly competitive market. This is what Lendmantra brings together: advanced conversational AI, robust loan management software for NBFC, and next-generation digital lending platforms into a cohesive framework designed for 2026 and beyond.

In a market where attention is scarce and trust is priceless, engagement defines success. And in 2026, engagement begins with intelligent conversation. To know more, contact us at info@solzit.com.

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

How does conversational AI improve borrower engagement?

It improves engagement by providing instant, accurate responses and 24/7 assistance. Borrowers receive timely updates, guided support, and quicker resolutions, which reduces confusion and builds trust throughout the lending journey.

How does conversational AI personalize borrower communication?

It analyzes borrower data such as repayment history and interaction patterns to deliver tailored recommendations, reminders, and support. This ensures communication remains relevant and context-specific.

Can conversational AI integrate with CRM and lending platforms?

Yes. Modern systems integrate seamlessly with CRM tools and digital lending platforms, enabling synchronized data access, automated workflows, and consistent borrower communication across departments.