Today, digital lending platforms are no longer a niche innovation—they are reshaping credit access, risk management, and portfolio growth across emerging markets in Africa, Asia, Latin America, and beyond. For lenders, this shift represents a powerful opportunity to expand reach, reduce costs, and serve previously underserved segments while navigating new competitive and regulatory realities.

Global digital lending markets are experiencing explosive growth. The sector was valued at around USD 10-13 billion in 2024 and is projected to reach USD 39-44 billion by 2030-2033, with CAGRs often cited in the 20-27% range (Source). Asia-Pacific is leading the charge as the fastest-growing region, driven by smartphone proliferation, rising internet penetration, and supportive policies for financial inclusion. Africa stands out with particularly strong momentum in mobile-first models, while Latin America continues to see robust fintech expansion addressing gaps left by traditional banking.

In markets like India, digital lending volumes have surged, with fintechs playing a key role in disbursing billions while helping close massive SME credit gaps. Similar stories are unfolding across Southeast Asia, Nigeria, Kenya, Brazil, Mexico, and other high-potential regions.

In this blog, we will explore the key drivers and emerging trends on digital lending in emerging economies, insights that will help forward-thinking lenders understand the transformative potential of the digital wave.

What Are Digital Lending Platforms?

| Aspect | Digital Lending | Traditional Lending |

| Processing Model | Automated | Manual |

| Documentation | Digital-first | Paper-heavy |

| Accessibility | Anytime, anywhere | Branch-dependent |

| Decisioning | Data-driven | Conventional review |

| Operational Cost | Operational Cost | Higher |

| Scalability | High | Limited |

| Customer Experience | Streamlined | Slower and fragmented |

Digital Lending vs Traditional Lending

Digital lending platforms are technology-enabled systems that allow lenders to manage the end-to-end lending lifecycle through digital channels.

These platforms eliminate many of the manual processes traditionally associated with lending by automating critical stages such as borrower onboarding, verification, underwriting, approval, disbursement, and repayment management. At the heart of these systems are digital lending solutions that integrate automation, analytics, APIs, and cloud infrastructure to create a connected lending environment.

Unlike traditional lending systems that often depend heavily on human intervention, digital lending platforms are built for speed, consistency, and scalability. For lenders, this means improved efficiency. For borrowers, it means easier access to financial services.

Why Are Emerging Markets Leading This Growth?

Emerging economies have become the fastest-growing markets for digital lending. This is largely because these regions have a significant credit access gap. Millions of individuals and small businesses remain underserved by traditional financial institutions due to limited formal credit history, geographic barriers, or operational inefficiencies within conventional banking systems. Digital lending technology is helping bridge this gap.

1. Rising Smartphone Penetration

The widespread availability of affordable smartphones has dramatically increased access to digital financial services. Borrowers can now apply for credit directly through mobile apps without visiting a branch. This mobile-first model is especially important in semi-urban and rural areas where physical banking access may be limited.

2. Government-Led Digital Infrastructure

Several emerging economies have invested heavily in digital infrastructure.

In India, initiatives such as Aadhaar-based identity verification, UPI-enabled payments, and digital KYC systems have created a strong foundation for digital lending platforms in India. Regulatory guidance from the Reserve Bank of India has further encouraged transparency and borrower protection. These frameworks have made digital lending adoption more scalable and trustworthy.

3. Demand For Faster Financial Services

Consumer expectations have evolved. Borrowers now expect financial products to match the convenience of digital commerce. Long approval cycles and branch-dependent processes no longer meet market expectations. This demand has accelerated the adoption of digital lending solutions among lenders looking to stay competitive.

Key Drivers Fueling the Rise of Digital Lending in Emerging Markets

Several powerful forces are converging to accelerate the adoption of digital lending platforms across emerging economies. For lenders and decision-makers, understanding these drivers is essential to identify where the biggest opportunities — and risks — lie.

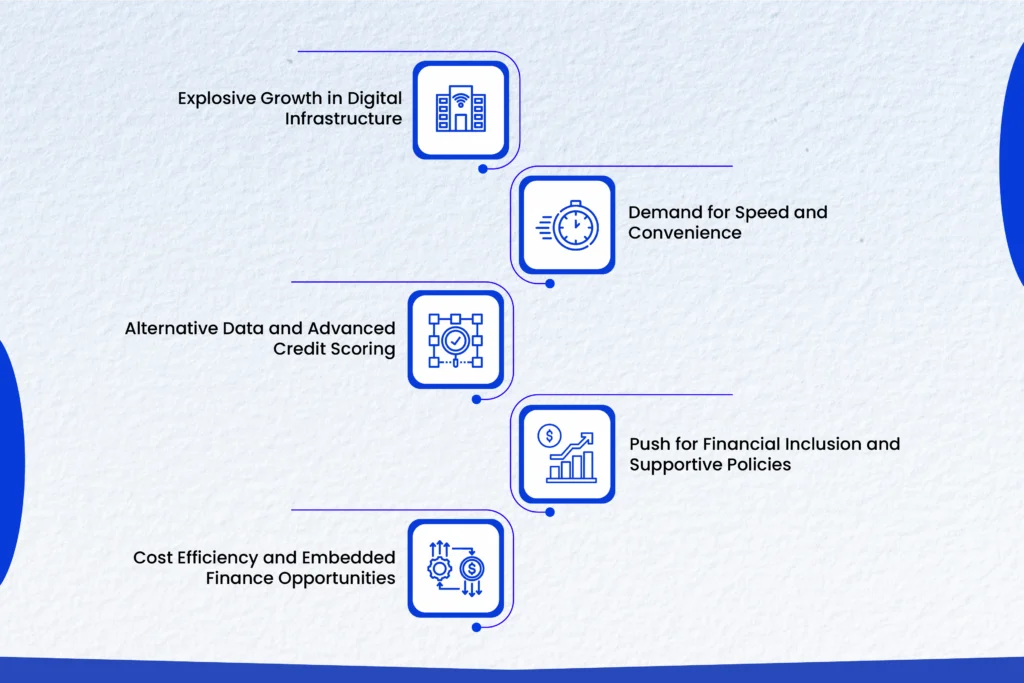

1. Explosive Growth in Digital Infrastructure

Smartphone penetration and internet connectivity have surged, creating the foundation for scalable lending. Mobile devices now serve as the primary gateway to financial services in many regions. In Africa and parts of Asia, mobile-first models allow lenders to reach remote and rural populations that traditional branches could never serve profitably. This digital infrastructure leapfrog has dramatically lowered customer acquisition and servicing costs while enabling instant loan applications and disbursements.

2. Demand for Speed and Convenience

Today’s borrowers — especially SMEs, gig workers, and younger consumers — expect credit decisions in minutes, not weeks. Digital platforms meet this demand with streamlined, paperless processes, real-time approvals, and seamless mobile experiences. This shift from slow, branch-based lending has unlocked massive latent demand, particularly for short-term working capital and emergency loans.

3. Alternative Data and Advanced Credit Scoring

Traditional credit bureaus often exclude large portions of the population in emerging markets. Digital lenders are closing this gap by leveraging alternative data sources — mobile usage patterns, transaction histories, e-commerce behavior, utility payments, and even psychometric data. Powered by AI and machine learning, these models deliver more accurate risk assessments for thin-file and unbanked borrowers, expanding the addressable market while improving portfolio performance.

4. Push for Financial Inclusion and Supportive Policies

Governments across India, Kenya, Brazil, Indonesia, and many other markets are actively promoting digital finance through regulations, open banking initiatives, and financial inclusion mandates. These policies encourage innovation while pushing traditional institutions to partner with or adopt digital solutions. The result is a more enabling environment for scalable lending.

5. Cost Efficiency and Embedded Finance Opportunities

Digital platforms significantly reduce operational overheads compared to legacy systems. This efficiency allows competitive pricing and higher margins. Additionally, the rise of embedded finance — integrating credit directly into e-commerce, payroll, utility, or supply chain platforms — is creating new distribution channels and recurring revenue opportunities for lenders.

The Role of Digital Lending Platforms in Emerging Markets

Digital lending platforms have moved from being mere technology providers to becoming critical enablers of financial inclusion, operational efficiency, and credit market expansion in emerging economies. For lenders and decision-makers, they serve multiple strategic roles that go far beyond simply digitizing loan processes.

1. Democratizing Access to Credit

- Digital platforms reach unbanked and underbanked populations — including small businesses, gig-economy workers, rural entrepreneurs, and low-income households — and are expanding the overall credit market.

- In India alone, digital lending has helped channel billions of dollars to SMEs that previously had limited access to formal credit.

- Similar impacts are visible across Kenya’s mobile lending ecosystem, Brazil’s instant credit sector, and Indonesia’s growing fintech landscape.

2. Transforming Credit Decisioning and Risk Management

One of the most valuable roles is the ability to make faster, smarter, and more inclusive credit decisions. Using alternative data, AI-powered scoring models, and real-time analytics, digital platforms assess creditworthiness beyond traditional credit scores. This results in:

- Higher approval rates for thin-file borrowers

- Lower default rates through continuous risk monitoring

- Better portfolio diversification

Lenders partnering with or adopting these platforms gain a significant competitive edge in both risk-adjusted returns and customer acquisition.

3. Driving Operational Efficiency and Cost Reduction

- Digital lending platforms drastically cut the cost of loan origination, underwriting, disbursement, and collection.

- This efficiency allows lenders to offer smaller ticket sizes profitably and serve high-volume, low-margin segments that were previously unviable.

4. Enabling Embedded Finance and New Business Models

- Modern digital platforms are powering embedded lending — seamlessly integrating credit into non-financial platforms such as e-commerce, supply chain systems, ride-hailing apps, and payroll solutions.

- These platforms create new distribution channels for lenders and improve customer experience by delivering credit at the point of need.

5. Catalyzing Innovation and Competition

- By introducing agile technology, data-driven products, and customer-centric design, digital lending platforms are forcing the entire financial ecosystem to evolve.

- Traditional banks and NBFCs are increasingly collaborating with these platforms through co-lending, white-label solutions, or technology adoption — accelerating modernization across the industry.

In essence, digital lending platforms are playing a dual role: they act as disruptors challenging legacy systems and as enablers helping established lenders scale, reduce costs, and reach new customer segments more effectively.

How Digital Lending Infrastructure Works?

The success of digital lending depends on a strong technological framework.

Behind every smooth borrower experience is a multi-layered system working together to process, assess, approve, and manage loans.

1. Borrower Interface Layer

This is the customer-facing layer.

It includes:

- Mobile applications

- Online lending portals

- Borrower dashboards

This layer allows applicants to submit information, upload documents, and track application progress. A well-designed interface improves borrower completion rates and reduces drop-offs.

2. Processing Layer

This layer handles application processing and workflow automation.

It is powered by a loan origination system that manages:

- Application intake

- Data collection

- Verification workflows

- Underwriting processes

- Approval routing

This is where loan originating software becomes essential. It automates tasks that traditionally required significant manual effort.

3. Intelligence Layer

This layer enables advanced decision-making. Using AI in lending, platforms can assess borrower eligibility, analyze risk, detect fraud patterns, and improve underwriting precision. It is this intelligence layer that allows digital lending technology to go beyond basic automation.

4. Servicing Layer

Once funds are disbursed, the servicing layer takes over.

This is powered by a loan management system that handles:

- Repayment scheduling

- EMI tracking

- Delinquency alerts

- Collections management

- Loan closure

5. Integration Layer

Digital lending platforms connect with external systems through APIs.

These integrations typically include:

- Credit bureaus

- Payment gateways

- Banking networks

- Compliance systems

- Verification providers

Together, these layers create a seamless lending ecosystem.

Final Thoughts

The rise of digital lending platforms in emerging markets represents one of the most significant financial shifts of the modern era. By expanding credit access, improving risk decisioning, and driving operational efficiency, these platforms are unlocking new growth opportunities for lenders while advancing financial inclusion.

However, this transformation also brings notable challenges—regulatory uncertainty, data privacy concerns, cybersecurity threats, over-indebtedness risks, and the constant need for robust technology infrastructure. Success demands a balanced approach that blends innovation with strong risk controls, responsible lending practices, and customer-centric design.

At Lendmantra, we understand the complexities of the lending landscape. Our AI-powered digital lending solutions are designed to help non-banking financial companies (NBFCs), fintechs, and financial institutions streamline the entire loan lifecycle—from origination and credit decision-making to disbursement and management. We ensure that our clients remain agile in ever-changing markets. If you’re looking for a comprehensive digital lending platform that meets all your needs as a lender, feel free to reach out for a free demo and trial.

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

Which countries are leading in digital lending adoption?

Countries like India, China, Indonesia, Kenya, and Brazil are leading in digital lending adoption due to strong mobile penetration, fintech growth, supportive regulations, and increasing demand for accessible credit solutions.

How do digital lending platforms improve financial inclusion?

They provide credit access to underserved individuals and small businesses using alternative data and simple processes. This helps people without a formal banking history participate in the financial system more easily.

How does AI improve credit risk assessment in digital lending?

AI analyzes large datasets like transaction history and behavior patterns to assess borrower risk. It improves accuracy, reduces bias, detects fraud, and enables faster, data-driven lending decisions.

How will digital lending evolve with AI and automation?

Digital lending will become faster, more personalized, and efficient. AI and automation will improve risk assessment, reduce manual work, enhance customer experience, and enable scalable, data-driven lending operations.