Borrowing money today doesn’t work the way it used to. What once involved multiple forms, back-and-forth communication, and long approval timelines has now shifted to faster, more digital-first processes. But while the front-end experience has improved, many lenders are still dealing with operational challenges behind the scenes.

Applications coming from multiple channels, manual verification steps, disconnected systems, and delays in decision-making continue to slow down the lending process. This is where the real pressure lies—not just in acquiring customers, but in processing them efficiently.

Today, digital lending is no longer just about offering online applications. It’s about seamless loan origination that ensures how smoothly and accurately a lender can move an application from submission to approval. A loan origination system (LOS) captures applications and defines how applications are verified, evaluated, processed, and approved across the entire lifecycle.

In this blog, we’ll look at what makes a Loan Origination System effective today, where traditional setups fall short, and what lenders need to stay competitive in an increasingly fast-moving lending environment.

- What Is A Loan Origination System?

- Why Modern Lenders Depend On Loan Origination Systems In 2026?

- How A Loan Origination System Manages The Lending Lifecycle?

- LOS-Enabled Application Intake And Borrower Onboarding

- Automated Verification And Document Management

- Intelligent Credit Decisioning Through LOS

- Workflow Automation And Operational Efficiency

- Integration And Data Connectivity In Modern LOS Platforms

- What Features Lenders Should Look For In An LOS?

- Final Thoughts

- Frequently Asked Questions

What Is A Loan Origination System?

A Loan Origination System (LOS) is software that manages the entire loan application lifecycle from the moment the borrower submits the application until the loan is approved and funded.

It brings together several lending activities such as:

- Application intake

- Identity and document verification

- Credit assessment and underwriting

- Decision and approval

- Documentation and financing

Instead of handling these steps manually or with different tools, a loan origination system centralizes them in a single platform, allowing lenders to process applications faster and with more accuracy.

Traditional vs Modern Loan Origination

| Traditional Lending Process | LOS-Enabled Lending Process |

| Paper-based applications | Digital application intake |

| Manual verification | Automated verification |

| Slow underwriting cycles | Real-time credit decisioning |

| Multiple disconnected systems | Unified LOS workflow |

| Weeks for approval | Minutes or hours for approval |

In simple terms, a loan origination system transforms lending operations from fragmented manual workflows into a structured digital process.

Why Modern Lenders Depend On Loan Origination Systems In 2026?

The expectations of borrowers and regulators have changed dramatically. Lenders must make quick decisions while maintaining strict risk and compliance standards.

A modern loan origination system helps lenders achieve this balance by combining automation, data integration, and workflow management.

Major changes in the industry include:

- The demand for instant approval of digital loans is increasing

- High expectations for seamless borrower engagement

- Increased requirements for compliance with the regulations

- Extend AI-powered credit decisions

- Greater reliance on data-driven underwriting

These changes mean lenders can no longer rely on manual processes or outdated software. Instead, they need a robust loan origination system that supports scalable digital loan operations.

How A Loan Origination System Manages The Lending Lifecycle?

One of the biggest advantages of a loan origination system is its ability to orchestrate the entire lending process in a structured workflow.

Key Stages Managed by an LOS:

| Lending Stage | How does a Loan Origination System enable it? |

| Application Intake | Captures borrower data through digital forms and portals |

| Verification | Integrates KYC, document verification, and fraud checks |

| Credit Evaluation | Pulls bureau data and financial records for analysis |

| Decisioning | Uses rule engines or AI models to approve or reject applications |

| Documentation | Generates contracts and manages document storage |

| Funding | Completes loan disbursement and handoff to servicing systems |

This structured workflow ensures that every loan application follows a consistent and auditable process.

Did you also know that the use of AI in lending allows lenders to analyze large volumes of borrower data and make faster, more accurate credit decisions?

LOS-Enabled Application Intake And Borrower Onboarding

The first step in lending is collecting borrower information. In traditional systems, this stage involved paperwork, repeated data entry, and long processing times.

A loan origination system simplifies application intake through digital onboarding tools, which improves the borrower onboarding through:

- Online and mobile application forms

- Auto-filled data from integrated sources

- Digital document uploads

- OTP verification and identity validation

- Real-time application tracking

These capabilities make the application process easier for borrowers while reducing operational effort for lenders.

Many LOS platforms also support multi-channel applications, allowing borrowers to search through websites, mobile apps, branches, or partner digital lending platforms without disrupting their workflow.

This provides a better borrower experience and fewer incomplete applications.

Automated Verification And Document Management

Once an application is submitted, lenders must verify the borrower’s identity, income, and financial documents.

Manual verification can be slow and error-prone. A loan origination system automates this stage through integrations and digital tools.

Major Verification Capabilities in an LOS

- OCR-based document extraction

- Identity verification integrations

- Fraud detection checks

- Automated income validation

- Centralized document storage

These features ensure that borrower data is captured accurately and securely.

Another advantage is centralized document management, where all application documents are stored in a structured repository. This improves transparency, simplifies audits, and prevents data duplication.

Intelligent Credit Decisioning Through LOS

One of the most powerful capabilities of modern loan origination systems is automated credit decisioning.

Traditionally, underwriting teams reviewed applications manually, which often took days or weeks. Today, LOS platforms integrate decision engines that evaluate borrower eligibility in real time. A loan origination system can analyze multiple data points, such as:

- Credit bureau scores

- Bank transaction data

- Income verification

- Alternative data sources

Using predefined rules or AI models, the system can generate loan decisions instantly or route complex cases to human underwriters. This leads to –

- Faster loan approvals

- Consistent credit policies

- Reduced manual errors

- Improved risk assessment

In 2026, AI-driven decisioning is becoming a key feature in modern LOS platforms, helping lenders process large volumes of applications efficiently.

Workflow Automation And Operational Efficiency

Another significant advantage of a loan origination system is the automation of the workflow.

There are several parties involved in the process of loan origination, such as loan officers, underwriters, and operational personnel. It is complex to coordinate all the parties without an automated system.

An advanced LOS arranges all the activities in an automated workflow.

Example Workflow In An LOS

- Borrower submits application

- LOS verifies identity and documents

- System runs credit checks

- The decision engine evaluates eligibility

- Underwriter reviews flagged cases

- Loan is approved and documentation generated

- Loan moves to funding stage

Each step triggers the next automatically, ensuring that no application is lost or delayed.

Operational Benefits

- Faster processing times

- Reduced operational workload

- Improved transparency

- Clear audit trails

By streamlining operations, a loan origination system enables lenders to handle higher application volumes without increasing staff.

Looking to streamline lending operations? Take control of your lending workflows and accelerate approvals with LendMantra’s smart loan origination system.

Integration And Data Connectivity In Modern LOS Platforms

Modern lending ecosystems rely heavily on data. A loan origination system must integrate seamlessly with external systems and data providers.

Typical integrations include:

- Credit bureaus

- KYC and identity verification providers

- Bank statement analyzers

- Payment gateways

- Core banking systems

These integrations allow the LOS to pull real-time data, making underwriting faster and more accurate.

Many modern platforms also follow API-first architectures, enabling lenders to connect their LOS with other fintech tools and lending infrastructure.

This level of connectivity is essential for digital lending operations that depend on continuous data exchange.

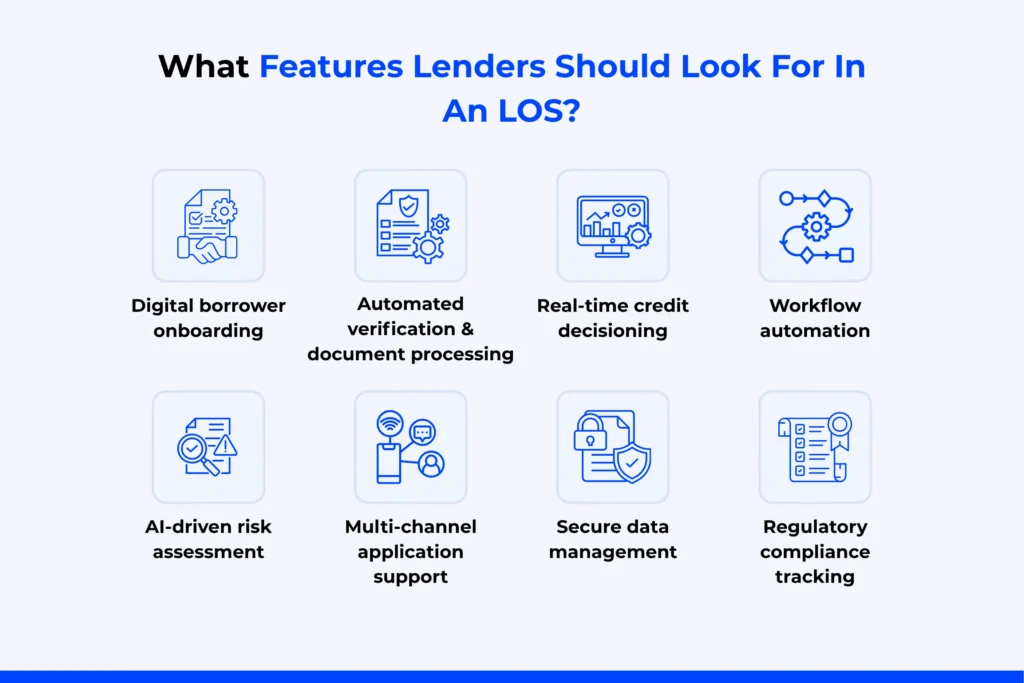

What Features Lenders Should Look For In An LOS?

When evaluating a loan origination system, lenders should focus on capabilities that support both efficiency and scalability.

Essential Features of a Modern LOS

- Digital borrower onboarding

- Automated verification and document management

- Real-time credit decisioning

- Workflow automation

- AI-driven risk assessment

- Multi-channel application support

- Secure data management

- Regulatory compliance tracking

These features ensure that the system can support evolving lending requirements while maintaining operational stability.

Final Thoughts

The lending enterprise is moving towards fully virtual, data-driven methods. In this environment, handling loan applications through manual workflows or disconnected systems is no longer realistic.

A cutting-edge mortgage origination system does a good deal more than method packages. It connects borrower onboarding, verification, underwriting, and decisioning right into a single operational framework.

By centralizing these abilities, an LOS turns into the operational backbone of modern lending, ensuring pace, accuracy, compliance, and scalability.

For lenders in 2026 and beyond, investing in an effective mortgage origination system isn’t always just a technology improvement. It is a strategic pass that determines how effectively they can compete inside the evolving digital lending ecosystem. If you are looking a modern, reliable, and secure loan origination system for your organization, then you may check LendMantra’s LOS and even LMS system and get a free demo to see its transforming capabilities.

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

What role does automation play in modern loan origination platforms?

Automation handles tasks like data entry, document verification, underwriting, and approvals, reducing human errors and delays, enabling consistent and scalable operations across modern digital lending platforms and loan originating software systems.

How do AI and data analytics enhance loan origination systems?

AI in lending analyzes borrower data, predicts credit risk, detects fraud, and enables smarter underwriting. While data analytics improves decision-making, customised approval rates across both consumer and commercial loan origination systems.

How does a cloud-based loan origination system benefit digital lenders?

Cloud-based systems offer scalability, remote access, lower investments in infrastructure costs, real-time updates, and seamless integrations, enabling digital lending solutions to integrate efficiently, adapt quickly, and deliver more reliable lending experiences.

How can lenders migrate from legacy lending systems to a modern LOS platform?

Lenders can migrate by assessing current gaps, choosing scalable digital lending platforms, ensuring data migration, integrating APIs, training teams, and adopting phased implementation to minimize disruption and improve overall lending performance.