Embedded finance has become one of the most consequential shifts in how credit reaches customers. Rather than a customer recognizing a need and approaching a lender, the platform itself identifies the need and presents credit at the moment it becomes relevant.

A small business owner using accounting software receives a pre-approved working capital offer based on their cash flow. A ride-sharing driver accesses vehicle financing through the same app they drive for every day. In each case, the lender isn’t waiting for the customer to come looking — the platform surfaces credit on its own terms, using its own data.

This is what’s driving lending beyond traditional channels and into the platforms people already trust and use. According to FIS, embedded finance is becoming an important distribution model for delivering seamless, integrated financial experiences, rather than standalone financial journeys.

But how exactly are banks, fintechs, and platforms positioning themselves within embedded finance: who originates the relationship, who carries the risk, and who the customer ultimately trusts? That’s what the blog examines.

- What Is Embedded Lending?

- The Ecosystem Behind Embedded Lending

- Why Is Lending Moving Beyond Banks?

- The Technology Behind Embedded Lending

- Real-World Examples Of Embedded Lending

- Embedded Lending In India: A Growing Opportunity

- Challenges And Considerations

- Strategic Recommendations For Winning In Embedded Lending

- Final Thought

- Frequently Asked Questions

What Is Embedded Lending?

Embedded lending is the integration of credit products directly into non-financial platforms — e-commerce sites, accounting software, marketplaces, mobility apps — so that borrowing happens inside the customer’s existing workflow rather than as a separate destination.

This differs from simply digitizing a bank’s application process. A bank that moves its loan form online has made lending faster; it hasn’t embedded anything. Embedded lending changes who initiates the credit relationship and where the underwriting data comes from. The platform, not the borrower, often surfaces the offer, and the decision is frequently based on data the platform already holds — transaction history, cash flow, sales velocity — rather than on a credit application filled out from scratch.

Three structural models account for most of what’s currently live in the market:

• Bank-as-a-service (BaaS): a licensed bank provides the balance sheet and regulatory cover; a platform or fintech owns the customer interface.

• Direct lending by the platform: a platform holds its own lending license (or operates through an NBFC) and carries the credit risk itself.

• Marketplace/referral lending: the platform surfaces offers from multiple lenders and is compensated for origination, without holding risk.

Which model a given embedded lending program uses determines who’s accountable for compliance, who absorbs losses, and how the economics are split — a distinction that matters more to financial institutions evaluating a partnership than to the end customer experiencing it.

The Ecosystem Behind Embedded Lending

While embedded lending appears seamless from a customer’s perspective, several players work behind the scenes to make these experiences possible.

- Banks and Financial Institutions: Provide the capital, manage regulatory obligations, and bring expertise in risk management and compliance.

- Fintech Providers: Build the technology infrastructure that enables quick integrations, automated decision-making, and smooth user experiences.

- Digital Platforms: E-commerce sites, marketplaces, accounting software providers, and other businesses act as a distribution channel, offering credit within existing customer journeys.

- Customers and Businesses: Access financing when they need it, without leaving the platform they are using.

This collaborative model highlights that lending may be moving beyond traditional banking channels, but banks remain an essential part of the ecosystem.

Why Is Lending Moving Beyond Banks?

Lending is moving beyond banks because customers increasingly expect fast, convenient, and seamless experiences within the digital platforms they already use. At the same time, advances in technology and data analytics enable businesses to offer timely and personalized credit solutions outside traditional banking channels.

- Customers Expect Convenience

Consumer expectations have evolved. Customers can order groceries, book travel, and stream entertainment instantly. Naturally, they expect financial services to offer the same level of simplicity.

Lengthy application forms and delayed approvals often create friction. Embedded lending removes these barriers by presenting relevant offers when customers need them.

Convenience is more than a differentiator; it is increasingly a requirement.

- Businesses Already Have Customer Relationships

Non-financial platforms interact with customers frequently. E-commerce marketplaces understand shopping habits. Software platforms know how businesses operate. Mobility apps track user behavior over time.

As these companies have established relationships, they are well-positioned to introduce financial products in familiar environments.

This shift changes the traditional distribution model. Instead of waiting for customers to approach them, lenders can reach borrowers through the platforms they already trust.

- Data Enables Better Decisions

One of the biggest advantages of embedded lending is access to contextual data.

A marketplace can assess a seller’s performance through transaction history.

Subscription software can evaluate recurring revenue patterns. Payment platforms can analyze cash flow trends.

This information supports informed decisions compared to relying solely on conventional credit assessment methods.

- Speed Has Become A Competitive Advantage

In any situation, timing matters as much as access to credit itself.

A retailer preparing for a seasonal surge may need immediate working capital. A customer purchasing an essential household appliance may not have time for a lengthy approval process.

Organizations that deliver fast, frictionless experiences are increasingly gaining an edge in today’s lending landscape.

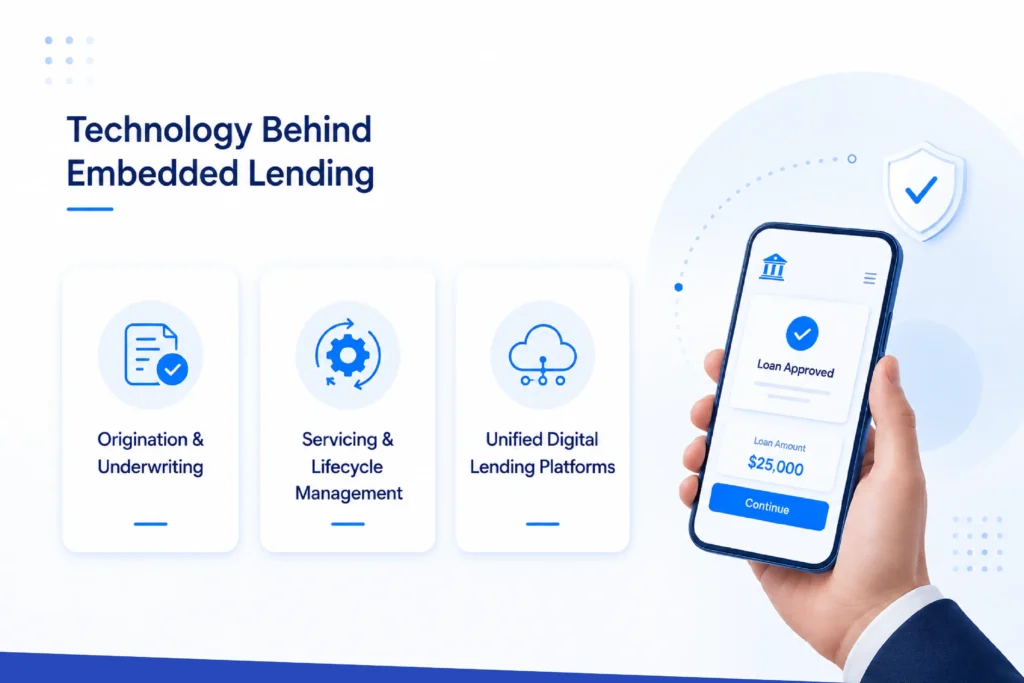

The Technology Behind Embedded Lending

Embedded lending depends on technology that can originate, manage, and service loans at a speed and scale manual processes can’t support. Most of this work falls into three stages of the lending lifecycle:

- Origination and Underwriting

Loan origination software automates data collection, eligibility checks, and verification, replacing manual paperwork with a structured workflow. Increasingly, the underwriting layer also pulls in alternative data — cash flow, transaction history, recurring revenue — sourced directly from the host platform’s API, which is what allows a credit decision to happen in seconds rather than days.

- Servicing and Lifecycle Management

Once a loan is disbursed, a loan management system handles repayment tracking, customer communication, and reporting. A broader lending management system ties origination, servicing, and compliance functions together, giving a lender visibility across the full loan lifecycle rather than siloed views at each stage.

- Unified Digital Lending Platforms

Many institutions are now consolidating these functions into a single digital lending platform that handles origination, underwriting, servicing, compliance, and analytics together. The advantage isn’t just operational efficiency — it’s the ability to launch new embedded lending products faster and adapt them as partner platforms and customer expectations change, without re-architecting the stack each time.

Real-World Examples Of Embedded Lending

Embedded lending is already widespread, even where the term itself isn’t visible to the end customer.

- Buy Now, Pay Later at Checkout

Perhaps the most visible example is Buy Now, Pay Later (BNPL). Instead of applying for a separate loan, shoppers can spread payments over several installments while completing their purchases.

The financing option becomes part of the checkout experience rather than an independent banking process.

- Seller Financing on Marketplaces

E-commerce marketplaces extend working capital to merchants based on sales performance and transaction history, replacing extensive documentation requirements with data the platform already has.

- Credit Through Business Software

Accounting and ERP platforms are beginning to offer financing sized to a business’s actual cash flow, rather than a generic loan amount based on a static application.

- Mobility And Travel Financing

Ride-sharing platforms, vehicle marketplaces, and travel companies are also embedding financial products into their services. Whether it’s vehicle financing for drivers or installment plans for vacation packages, lending is increasingly becoming contextual.

The common thread across all these examples is simple: credit appears when it is most relevant.

Embedded Lending In India: A Growing Opportunity

India’s digital transformation has created fertile ground for embedded finance. With widespread smartphone adoption, the rapid growth of digital payments, and initiatives that encourage financial inclusion, consumers have become more comfortable engaging with financial products through digital channels.

Small businesses, in particular, stand to benefit. Many MSMEs struggle to access formal credit due to limited documentation or lengthy approval procedures. Embedded lending addresses this directly by using transaction data and alternative signals — GST filings, payment gateway data, e-commerce sales history — to assess creditworthiness where a bureau score alone would fall short.

As adoption grows, digital lending platforms in India are likely to play an increasingly important role in expanding access to credit. By integrating lending into platforms that businesses and consumers already use, these solutions can help address long-standing financing challenges while creating more personalized borrowing experiences.

However, growth must be accompanied by responsible practices to ensure that convenience does not come at the cost of consumer protection.

Challenges And Considerations

Embedded lending offers real advantages, but it introduces risks that are distinct from those in traditional lending — and that financial institutions evaluating partnerships should weigh carefully.

- Responsible Lending and Affordability

Easy access to credit can be empowering, but it can also lead to over-borrowing if affordability assessments are not robust. Lenders and platforms must ensure that speed does not compromise sound decision-making.

- Data Privacy and Customer Consent

Embedded lending often relies on customer data to generate insights and personalize offers. This raises important questions around transparency, consent, and how information is collected and used. Customers should understand why their data is being accessed and how it influences lending decisions.

- Regulatory Accountability

Regardless of which structural model is used — BaaS, direct lending, or marketplace referral — compliance obligations don’t disappear; they shift to wherever the risk sits. Clear accountability for who owns regulatory compliance in a multi-party embedded lending arrangement is essential, particularly as regulators in markets like India tighten scrutiny of digital lending practices.

- Balancing Convenience with Trust

Convenience drives adoption, but trust determines whether embedded lending relationships last. Institutions that are transparent about pricing, data use, and who they’re partnering with will be better positioned than those competing purely on approval speed.

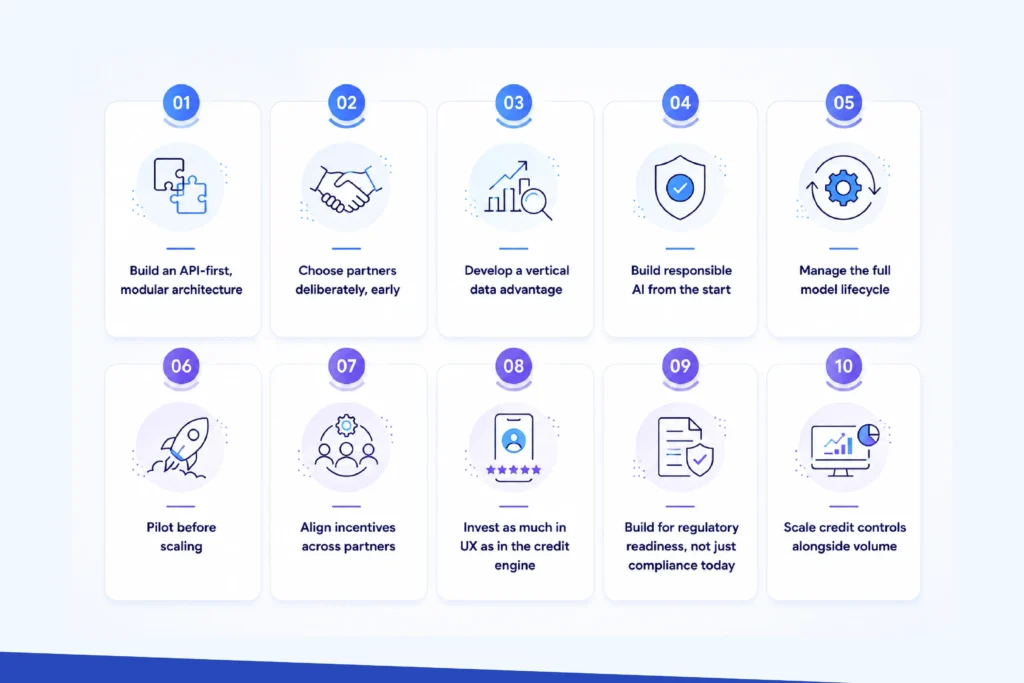

Strategic Recommendations For Winning In Embedded Lending

For banks, NBFCs, and fintechs building or partnering in this space, a few practices make embedded lending durable:

- Build an API-first, modular architecture: Treat credit assessment, risk evaluation, and disbursement as independent modules so individual components — including underlying AI models — can be upgraded without disrupting the full platform.

- Choose partners deliberately, early: If you lack lending licenses, regulatory expertise, or capital, partner with an established financial institution rather than trying to build all three at once — it reduces time to market and operational risk.

- Develop a vertical data advantage: Focus on sectors you understand deeply — e-commerce, agriculture, logistics — where industry-specific data meaningfully improves underwriting accuracy over generic credit models.

- Build responsible AI from the start: Explainability, bias testing, and audit trails are far cheaper to design in at the outset than to retrofit after a regulator or partner asks for them.

- Manage the full model lifecycle: Continuously monitor and retrain underwriting models as borrower behavior and market conditions shift; a model that was accurate at launch won’t stay that way without maintenance.

- Pilot before scaling: Start with smaller loan sizes or lower-risk segments, and use what you learn to refine policy before expanding exposure.

- Align incentives across partners: Set clear revenue-sharing and risk-sharing terms up front so every party in the value chain is incentivized toward portfolio quality, not just origination volume.

- Invest as much in UX as in the credit engine: A strong underwriting model can’t compensate for a confusing borrower journey — both need to be built with equal care.

- Build for regulatory readiness, not just compliance today: Bake data privacy and consumer protection requirements into the operating model from day one, since lending regulation in this space is still evolving.

- Scale credit controls alongside volume. Embedded lending enables growth at low marginal cost, but collections discipline and risk oversight need to scale at the same pace as origination, not after the fact.

Final Thought

Lending is no longer confined to bank branches, lengthy applications, or isolated financial interactions. Embedded finance is changing where and how people access credit, integrating lending into the digital experiences they use every day.

From online shopping and marketplace financing to software-driven credit solutions, borrowing is becoming more contextual and customer-centric. At the same time, technologies such as loan-originating software, loan management systems, and advanced digital lending solutions are enabling organizations to deliver these experiences at scale

As customer expectations continue to evolve, the organizations that thrive will be those that combine innovation with responsibility. Embedded finance platforms’ credit ratings are reshaping how lenders evaluate risk and scale lending operations. The real advantage is not in individual models but in the infrastructure that connects data, policy guidelines, workflows, and monitoring systems.

Banks and NBFCs that build such infrastructure shall be able to support quick lending decisions, with stronger risk management and sustainable growth in digital lending. To bring shifts that help you grow, you can get a free trial of LendMantra LOS and LMS systems that are designed to support digital lending with modern solutions. Contact us for a free trial.

Read More: https://lendmantra.com/blog/

Frequently Asked Questions

How is embedded finance transforming the lending industry?

Embedded finance shifts lending from traditional bank channels to digital experiences, enabling faster approvals, contextual credit offers, and more convenient borrowing journeys.

How do embedded lending solutions improve customer experience?

Embedded lending solutions simplify borrowing by reducing paperwork, speeding up approvals, and offering credit at the point of need within familiar platforms.

What are the benefits of embedded finance for lenders and businesses?

Embedded finance helps businesses generate new revenue streams, strengthen customer relationships, expand reach, and improve credit accessibility through digital channels.

How does embedded lending reduce friction in the borrowing process?

Embedded lending minimizes multiple application steps, automates decisions using real-time data, and eliminates the need to switch between platforms.

How does embedded finance support small lending businesses?

Embedded finance enables small lenders to scale efficiently, reach new customers, automate operations, and compete through technology-driven lending experiences.

What are the challenges associated with embedded finance?

Key challenges include data privacy concerns, regulatory compliance, responsible lending practices, transparency in credit decisions, and preventing customer over-indebtedness.