- Do you know digital lending is booming with a projected $34.56 billion growth by 2028?

- The Key Players in Digital Lending

- The Role of FinTech in Reshaping Lending for Businesses

- Top Trends Shaping the Future of Lending in 2025

- Future-proof Lending Strategies for Financial Institutions

- Statics and Market Status in Digital Lending

- The Road Ahead

- Frequently Asked Questions

Do you know digital lending is booming with a projected $34.56 billion growth by 2028?

This blog delves into the future of digital lending and what you discover by the end might just leave you astounded. But remember, if you miss this, you are missing the advanced borrowing factors and opportunities, which can be your future finance savior.

From Paper to Pixels: The Digital Lending Revolution

Because traditional lending has always been challenging and concerning in India, netizens find it preferential and biased. The situation has become so inelegant that people consider digital lending a better yet more convenient option. To discuss the future of digital lending, it is important to comprehend what made people inclined towards digital lending technology in India.

With the expansion of tech-enabled services, the FinTech revolution in lending solutions has been remarkable. Primarily in the APAC, people are more indulged in mobile-based solutions which persuades them to shift towards innovative lending platforms. This is because technology and such FinTech features are capable of catering to different conditions and needs of different people.

Where traditional borrowing patterns were extremely time-consuming, automation in loan approvals has made the entire borrowing process effortless and uncomplicated. In 2025, AI and automation have eased the increasing public demand for improved services concerning their monetary flow. For a better understanding, let’s see the role of FinTech in reshaping lending for businesses and diverse entrepreneurial bodies.

The Key Players in Digital Lending

Since the FinTech expansion, smart lending systems cover a wider spectrum of lending requirements for all types of businesses. These platforms have also enhanced the borrower experience with automation in loan approvals, reduced paperwork, and customized lending solutions.

For the same reasons, NBFCs are collaborating with digital-first loan disbursement systems to deliver seamless lending services to businesses. Traditional banks have also started relying on cloud-based lending software to gain back relevancy in the market. The Last are the startups aiming to deliver fintech services to the underserved. Overall, when it comes to digital lending services, there are primarily three key players;

- Non-banking Financial Companies: To deliver an impeccable lending experience to businesses utilizing advanced technology.

- Traditional Banks: To retain their relevancy in the market.

- Startups: To bring niche and solutions to the marginalized market.

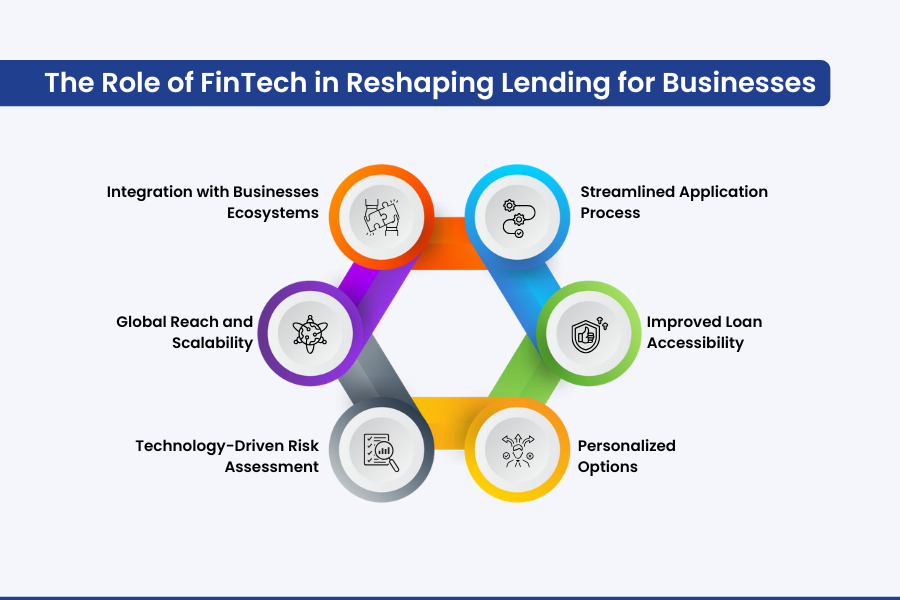

The Role of FinTech in Reshaping Lending for Businesses

With the exponential tech evolution, FinTech took no time, to form its space in the finance sector. The FinTech revolution in lending services became a reliable yet accustomed lending source for modern business needs. Here are certain factors that define how automation in loan approvals became a prominent aid in shaping the future of digital lending.

Streamlined Application Process:

Smart lending systems simplify loan approval by leveraging the online loan disbursement process. It reduces paperwork, processes applications faster, and takes less time for loan approvals. Moreover, it allows businesses with quick access to funds making the process uncomplicated.

Improved Loan Accessibility:

Unlike traditional loans, digital lending has better accessibility. FinTech has made the Online loan disbursement process accessible to underserved markets, startups, small businesses, or those with limited credit history. This better service difference is shaping the future of digital lending as one of the most reliable resources for borrowers.

Personalized Options:

Along with Financial inclusion through digital lending and data-driven insights, FinTech lenders can offer tailored loan options to enterprises. It allows businesses access to multiple lending options that cater to their specific business needs. These can be short-term loans, working capital solutions, or invoice financing.

Technology-Driven Risk Assessment:

With Artificial Intelligence and automation in loan approvals, FinTech lenders have better risk evaluation grounds. Through predictive analytics credit decisions, lending systems have the accuracy to reduce the defaulter’s risk.

Global Reach and Scalability:

Financial inclusion through digital lending has authorized people to experience fintech solutions despite their location. This has made borrowing and lending, easily accessible for growing businesses in remote areas.

Integration with Businesses Ecosystems:

One of the many benefits of automated lending is that many FinTech systems use advanced technology. It allows these lending platforms to seamlessly integrate with your FinTech features or tools, extending the system’s performance. This also delivers an enhanced user experience.

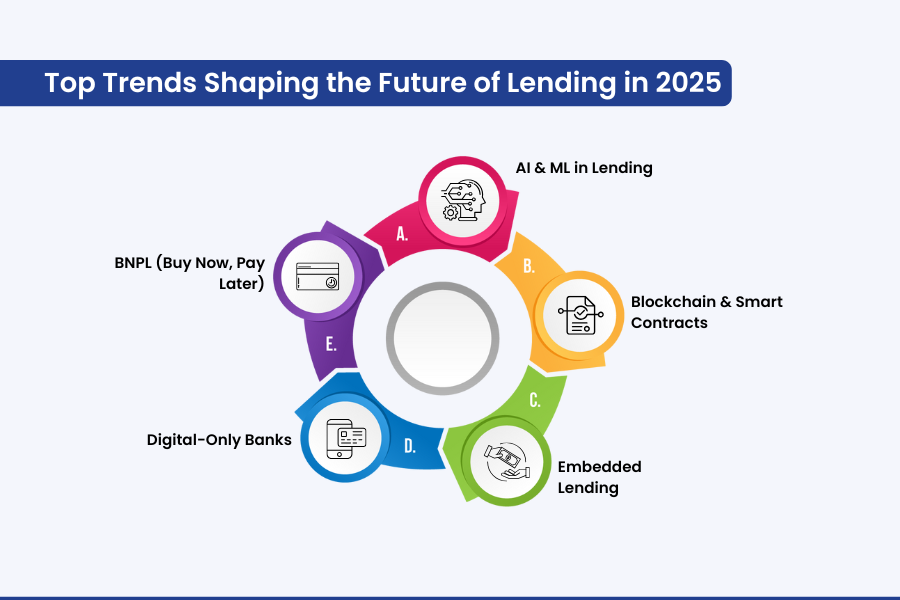

Top Trends Shaping the Future of Lending in 2025

With so much growth in the benefits of automated lending, let’s have a glimpse at the trendiest lending qualities. Here are the top trends shaping the future of lending in 2025:

AI and Machine Learning in Lending:

Artificial Intelligence and Machine learning (a subset of AI) encourage automated data-driven lending. Through advanced algorithms, AI and Machine learning lending offer crucial data analysis for potential prospects. It allows credit unions or NBFCs for fair automated loan disbursement with fair accounting.

Blockchain and Smart Contracts:

Blockchain in loan management helps record transactions across a computer network securely and transparently. Whereas, smart contracts are automated contracts that enforce agreements between a lender and borrower.

Embedded Lending:

If you have ever witnessed the “Buy Now, Pay Later” option, you were offered embedded lending where the loan is on the NBFC. It is a type of lending where the borrower gets credit on the merchant app without involving or moving to any third-party portal.

Digital-Only Banks and Neobanks:

Digital-only banks are the associated digital branches of established banks, primarily operated by traditional banks. Neobanks are digital-first finance companies that can operate unassisted or in partnership with traditional banks.

BNPL:

“Buy Now, Pay Later!” But do not confuse it with embedded lending. Although both finance solutions provide credit options, they vary in multiple aspects. It can be said to be one of the most visible forms of embedded lending, popular among online shoppers.

After multiple digital lending trends in 2025, do you know what are the efficient strategies shaping the future of digital lending? As NBFCs and credit unions are acknowledging that the existing lending culture is rapidly eradicating, they are visibly shifting toward the best and most reliable LMS like LendMantra. However, it is crucial to understand how this evolution is allowing such platforms to curate future-proof lending strategies for financial institutions.

Future-proof Lending Strategies for Financial Institutions

To maintain a visible status in the race for relevancy, NBFCs have started relying on top cloud-based lending software like LendMantra. Hence let’s explore some proven strategies to understand the factors that are shaping the future of digital lending in India.

Embedded Finance and FinTech:

Integrating financial services into nonfinancial platforms allows institutions to gain augmented access. With enhanced reach to new market segments, consumers are offered tailored lending solutions with Cloud-based lending software.

Enforcing Advanced Technology:

Leveraging AI or Automation in loan approvals can significantly reduce time consumption and enhance efficiency in loan approvals. For instance (as per resources), Sutherland’s intelligent automation solutions have accelerated loan cycles by 50% while reducing operational costs for leading U.S. financial institutions.

Integrating ESG Criteria:

Accomplishing the environmental, social, and governance criteria, can help in sustainable lending decision-making. Implementing centralized ECG criteria streamlines data, its management, and operations. It further allows lenders to have data-driven insights and cater to borrowers’ requirements with tailored benefits of automated lending.

Modernizing Applications:

Transforming root systems into modern advanced FinTech platforms with integrated features can improve user experience. It also helps with streamlined operations and improved service delivery.

Implementing Data-Driven Strategies:

Leveraging data-driven designs allows NBFCs or credit unions to deliver enhanced user satisfaction. With Real-time credit scoring solutions, FinTech platforms can deliver precise services to the users.

With the rapid growth in the Fintech industry and growing digital lending trends in 2025, Non-banking Financial Companies and credit unions are more focused on delivering financial inclusion through digital lending. Look at the below-mentioned data that demonstrates how Next-gen digital lending tools are building trust in the market.

Statics and Market Status in Digital Lending

Market Growth:

The digital lending market is projected to expand by $34.56 billion between 2023 and 2028, with a compound annual growth rate (CAGR) of 26.63% during this period. (resources)

Adoption of Web-based Applications:

As of 2024, 90% of financial institutions offer web-based loan applications, a notable increase from 75% in 2019. However, less than half of these institutions provide fully digital end-to-end lending processes, indicating room for further digital optimization. (resources)

Role of Physical Branches:

A survey revealed that 64% of respondents anticipated a reduced role for physical branches by 2024, as digital solutions become more prevalent. (resources)

Small Business in Lending:

Nearly 70% of banks reported a decline in small business loan demand in the first half of 2024, attributed to higher borrowing costs and economic uncertainties. Nonetheless, approximately 60% of small business owners expect their need for credit to increase in the next 12 months, highlighting a potential area for digital lending growth. (resources)

Consumer Preferences:

The percentage of consumers completing loan applications online decreased from 76% in 2021 to 57% in 2024, possibly due to increasing regulatory and security concerns. (resources)

The Road Ahead

The FinTech revolution in digital services is at its extreme pace! Where NBFCs and credit unions are adapting digital lending and automation in loan approvals, FinTech is already updating the existing versions. The data and facts prove explicitly there is no better credit solution than Next-gen digital lending tools like exceptional LMS by lendmantra.

With the best credit solutions, digital lending is merely time-consuming and offers tailored loan solutions with real-time credit scoring solutions. If you are someone stuck with traditional lending methods, attempt automated lending platforms for faster approvals.

Be the best and most reliable NBFC by integrating cloud-based lending software into your digital lending platform. But are these lending softwares reliable enough to be integrated? Not All! Hence, all you need is the best yet most reliable digital LMS like lendmantra!

Finance is the Future, and If you do not make smart moves now, you will probably miss the smartest monetary opportunities in the Future.

Frequently Asked Questions

Why is automation crucial for the future of lending?

Automation plays a significant role in digital lending. It has helped to make the most challenging lending tasks like verifying documents, evaluating credit worth, and loan approval, easier and quicker to be done. This has enhanced lending efficiency and allows lenders to serve a larger number of loan seekers. At the same time, it has eased lending for borrowers with lesser paperwork and faster access to funds.

How do digital lending platforms benefit borrowers?

Digital lending platforms foster unparalleled ease for borrowers. They simplify the application process, allowing borrowers to apply for loans digitally at their convenience. Moreover, these platforms often provide better interest rates and personalized loan options based on individuals' requirements and credit profiles. With multiple features like real-time tracking and easy repayment options, digital lending delivers an exceptional experience to both lenders and borrowers. ?

What is the role of FinTech in shaping modern lending?

FinTech companies have entirely revolutionized lending amalgamating technology with finance. Together they have come up with multiple innovations like fairer loan evaluations for people with lower credit histories, AI-based credit scoring, and much more. With the digital innovation in finance, lending has become more accessible to underserved communities through mobile-friendly platforms. These platforms provide custom lending services leveraging data analytics and being more inclusive and customer-specific.